Currency markets closed recently with a shift in tone, as investors all of a sudden found themselves rectifying on Fed’s easing path once again. The strength of the United States economic climate stunned lots of. Development, working with, and financial investment all showed more stamina than anticipated, fueling questions concerning whether policymakers absolutely need to speed up the pace of cuts. The inquiry currently is not whether the Fed will relieve in October, yet how much sentence remains for December and past.

That unpredictability aided knock the wind out of equity markets. After a record-breaking run, supplies lost energy as capitalists considered the possibility of a shallower relieving course. Treasury yields, in turn, prolonged their rebound, while Buck surged, gaining from both yield assistance and some safe-haven need.

Not all money fared equally in this recalibration. Swiss Franc and Euro took care of to publish gains, albeit a lot more decently than Buck. Both gained from constant reserve bank stances. Their strength, nevertheless, was as much concerning avoiding weakness as it had to do with authentic positive outlook.

At the various other end of the spectrum, commodity currencies struggled. Kiwi tumbled additionally on continual expectations of a big RBNZ cut and management transition at the reserve bank. Loonie slid regardless of GDP rebound, as underlying economic weakness left markets encouraged a lot more BoC relieving is on the horizon. Yen additionally damaged, pushed by yield differentials.

Aussie taken care of to being in the center, along with Sterling. Assistance originated from upside rising cost of living shock in Australia that pared back RBA cut bets, though sentence will eventually rest on quarterly CPI later on in October. Sterling, meanwhile, wandered, caught in between softer development information and speculation over how hawkish the BoE will transform.

The performance scoreboard tells the story plainly: Buck, Franc, and Euro at the top; Kiwi, Loonie, and Yen anchored near the bottom; and Aussie and Sterling captured in the center.

United States Data Resilience Tempers Fed Cut Wagers Past October

Expectations for Fed alleviating changed notably last week as a string of stronger-than-expected United States data challenged the case for hostile rate cuts. The upgraded Q 2 GDP print, resistant September PMIs, firmer jobless insurance claims, and robust durable goods orders underscored financial durability in spite of toll headwinds.

This recalibration left futures still valuing a near-certain October cut, however with much much less sentence for December. The change has rippled throughout markets: United States stocks lost momentum from document highs, Treasury returns expanded their rebound, and Dollar surged to end up the week as the toughest major currency.

The US economy continues to resist expectations. The final estimate for Q 2 GDP was changed up greatly to 3 8 % annualized, from 3 3 % formerly, showing that activity held firm in spite of tariff headwinds. Rather than reducing greatly, development brought strong energy into Q 3

PMI studies for September strengthened that strength. At 52.0 for production and 53 9 for solutions, both industries remain easily in development region. The composite information suggest result is broadening at a 2 2 % annualized rate this quarter, regular with a gradual as opposed to abrupt cooling.

Work signals have also steadied. Weekly out of work claims fell back listed below 220 k, a degree that indicates hiring is not collapsing. The settlement of reciprocal tariffs in August may be motivating companies to return to normal recruitment, easing fears of unexpected weak point in the labor market.

At the same time, consumer goods orders surged unexpectedly. Headline orders increased 2 9 % in August, led by a near- 8 % jump in transport equipment, while core steps also surprised to the upside. The numbers suggested that services still have confidence to invest in resources products, even amidst worldwide uncertainty.

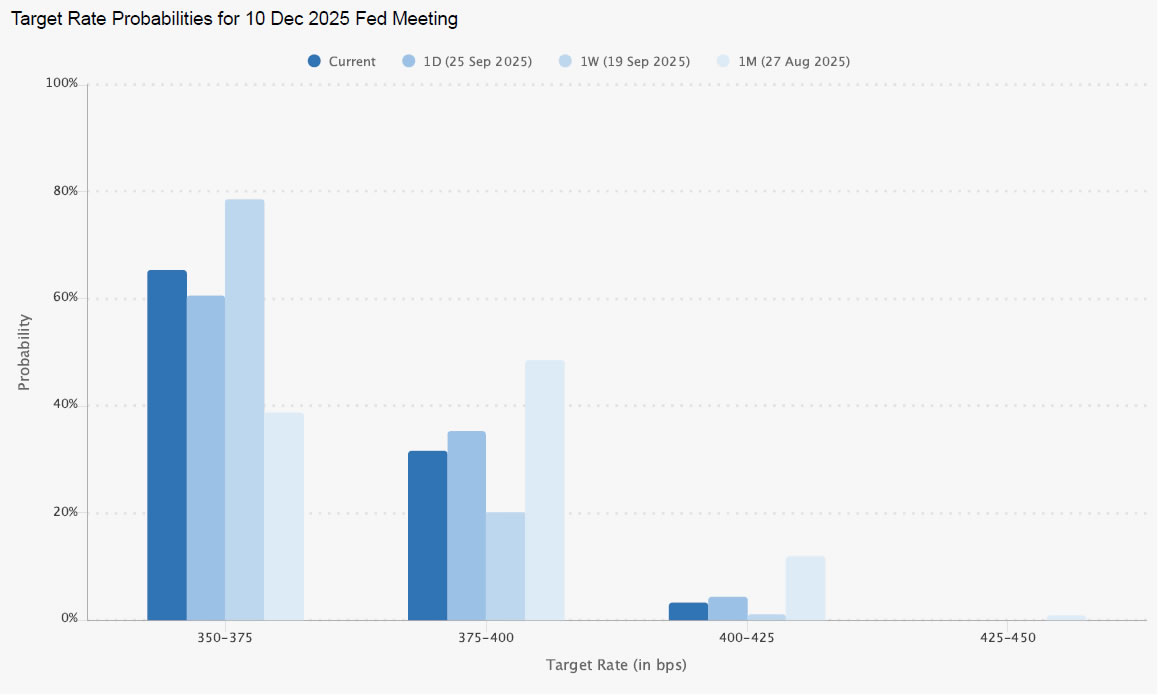

These strong data have changed market sights on the Fed. Futures continue to price a high likelihood– 87 7 %– of another cut in October, but bets on a December action have actually gone down to 65 4 %, well listed below virtually 80 % seen a week ago. The market message: an additional “insurance policy” cut is likely, yet an extensive alleviating cycle is much less specific.

Fed officials have mostly echoed that cautious stance. With the significant exemption of Governor Stephen Miran, who continues to suggest for much deeper cuts, many policymakers emphasize that policy decisions need to continue to be tied to the circulation of data. That setting has actually been enhanced by evidence of financial durability.

Still, threats stay. Fed Chair Powell recognized that job creation is sliding below the “breakeven” speed required to maintain unemployment consistent. If hiring deteriorates further, the Fed might still be required to accelerate easing in spite of the strong GDP background.

The September non-farm pay-rolls report will certainly be pivotal. A solid end result might verify the situation for a slower reducing pace, but a weak print would certainly press the Fed towards more “danger monitoring” decreases. Up until after that, expectations remain liquid, with markets balancing solid development against vulnerable employment signals.

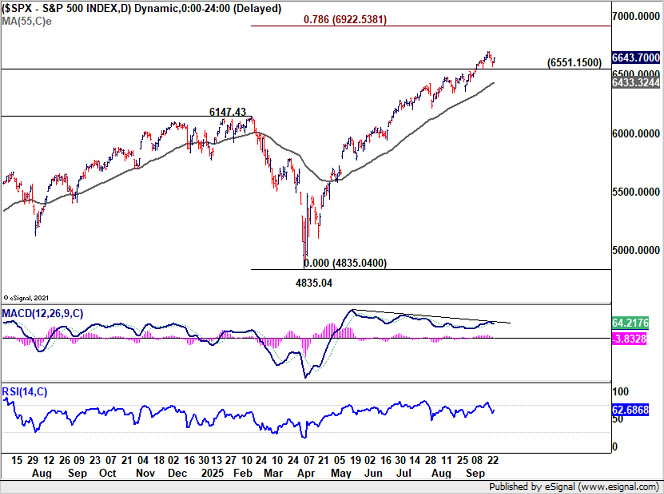

Equities Shed Momentum as Fed Wagers Reprice, Yet Uptrend undamaged

US equities lost some heavy steam recently as the stronger economic backdrop forced capitalists to reassess the degree of Fed reducing ahead. S&P 500 retreated from document highs, and the instant emphasis now drops on whether the index can hold over vital short-term support at 6551 15

Definitive break listed below this level would certainly validate near term covering and break the ice for a much deeper correction toward the 55 Day EMA (now at 643332 However, the broader uptrend continues to be intact, and strong acquiring passion should be anticipated on dips, with the EMA zone offering a cushion.

Alternatively, solid rebound from current levels would promptly shift sentiment back to the upside. S&P 500 can after that resume its rally toward 78 6 % projection of 3491 58 to 6147 43 from 4835 04 at 6922 53, extending the outstanding run that has specified much of 2025

The trajectory will certainly pivot heavily on the next round of labor and inflation data, which can either verify or test the market’s present positioning.

10 -Year Return Extends Rebound However 4 3 Must Cap

United States Treasuries sold off even more recently, with 10 -year return prolonging its rehabilitative rebound from the 3 992 reduced to close at 4 187 The move mirrors changing Fed expectations after the stronger run of financial data.

Technically, the return is currently looking at more increase to 55 D EMA (now at 4 215 and potentially over. However dropping channel ceiling near 4 300 need to give solid resistance to restrict upside, reinforcing the more comprehensive decline from 4 629 that continues to be intact.

On the downside, break back below 4 110 would suggest that the rebound has already run its training course, and placed the spotlight back on the 3 992 low.

Buck Index Rebound to Proceed as Short-term Bottom Created

Buck Index’s extensive rebound and break of 55 D EMA (now at 98 05 need to validate short-term bottoming at 96 21 Taking into consideration bullish convergence problem in D MACD, it’s possible that whole autumn from 110 17 has actually finished also. More increase is in currently prefer to as lengthy as 97 22 support holds, to 100 25 resistance.

However, the zone in between 38 2 % retracement of 110 17 to 96 21 at 101 54 and 55 EMA (now at 101 10 would be a substantial obstacle. It would needs either extended surge in yield with the dropping network, or prolonged adjustment in supplies, or both, to provide Dollar Index the fuel to overcome this resistance area.

On the other hand, break of 97 22 support will certainly dampen near term bullishness and bring retest of 96 21

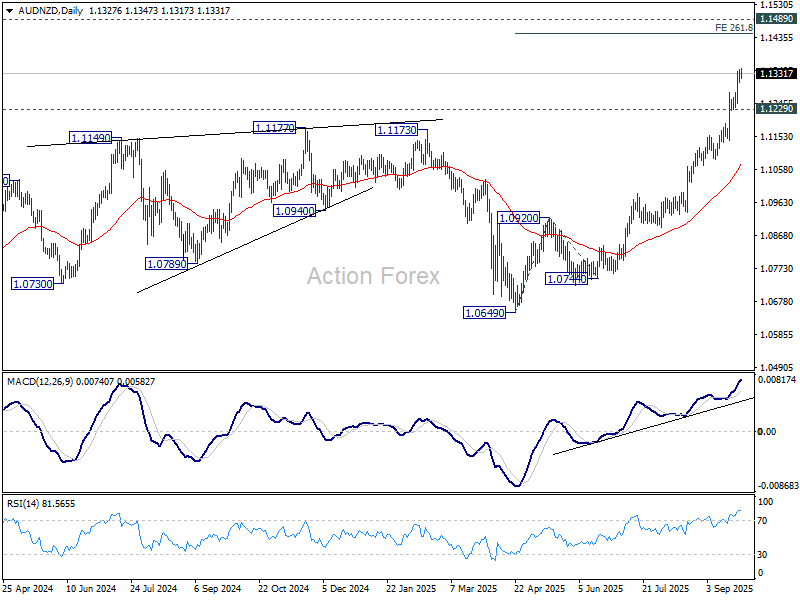

Kiwi and Loonie Battle, Aussie Flaring Somewhat Much Better

Product currencies battled last week, with New Zealand Dollar leading losses as markets braced for a more aggressive easing course. Weak residential information have currently built the case for a 50 bps RBNZ cut on October 8, and view was further clouded by uncertainty around a management adjustment at the reserve bank.

In a surprise statement, Swedish financial expert Anna Breman was called the next Guv of the RBNZ, readied to take office on December 1 Currently the First Replacement Guv at the Riksbank, Breman’s visit rated as bringing international experience, though it lugs little weight for the brewing plan conferences. She may go to November’s gathering as an observer, yet she will certainly not hold electing power.

The more prompt implication lies in the separation of Guv Christian Hawkesby, who tips down at the end of November. Markets presume that, provided his exit, Hawkesby may be less likely to vigorously shape consensus in the MPC. That might turn the equilibrium towards a bolder move in October, specifically with the economic climate under stress. Consequently, traders see climbing chances that the RBNZ will opt for a half-point cut at the next meeting.

Canadian Buck also underperformed, regardless of July GDP showing a 0. 2 % regular monthly rebound. It was the first growth in four months and offered some alleviation after a string of soft prints. Yet the positive outlook rapidly faded as advancement price quotes recommended August GDP was flat, emphasizing that any kind of healing is still vulnerable.

The composition of development revealed familiar obstacles. Goods-producing markets supplied the bulk of the gains, while retail trade pulled down the solutions side. Realty and wholesale activity showed some durability, but overall momentum remains tepid, and only just over half of all industries reported expansion.

Versus this backdrop, the BoC’s price reduced to 2 50 % previously this month looks even more like a first step than an option. Market babble has transformed to the chance of 2 more cuts prior to year-end, with October seen as a solid prospect for the next relocation. Weak company investment and recurring trade frictions with the United States amplify the demand for plan support.

Unlike its Kiwi and Loonie peers, Australian Dollar discovered some assistance recently after rising cost of living stunned on the advantage. August’s monthly CPI accelerated to 3.0%, above agreement expectations and pushing heading rising cost of living back to the top of the RBA’s 2– 3 % target band.

The stronger data triggered a sharp response in bonds, with three-year federal government yields jumping to the highest level because May. Cash markets quickly pared back expectations for a November RBA cut, pricing the chance of relieving listed below 40 % compared to over 60 % earlier in the week.

The RBA, nevertheless, is unlikely to modify its constant strategy. Guv Michele Bullock has actually emphasized that the Financial institution requires to stabilize motivating family spending with ensuring rising cost of living stays secured. That indicates the October 29 quarterly CPI will be decisive, with November’s plan decision still carefully balanced.

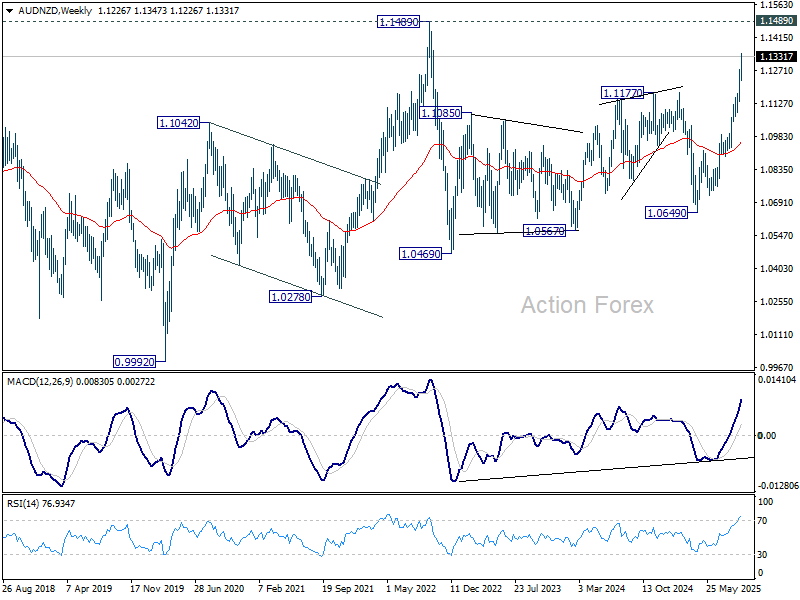

Technically, AUD/NZD remains in upside acceleration as seen in D MACD. Additional rally is expected as long as 1 1229 assistance holds. Current increase from 1 0649 is in progression for 261 8 % projection of 1 0694 to 1 0920 from 1 0744 at 1 1453 Nonetheless, 1 1489 (2022 high) must top upside, at the very least on first attempt.

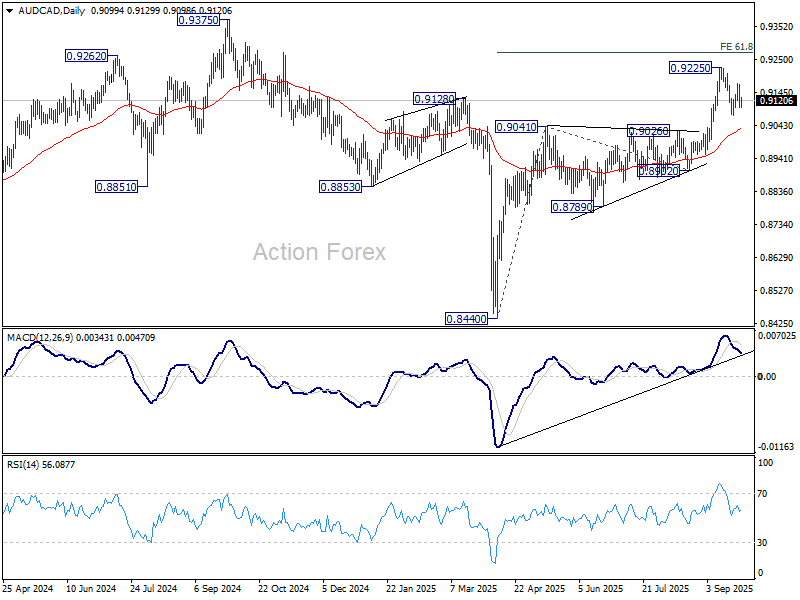

AUD/CAD ‘s rally was, nonetheless, was frustrating as the intra-week rally effort fell short well listed below 0. 9225 resistance. However, near term overview will certainly stay favorable as long as 0. 9041 resistance turned assistance holds. Increase from 0. 8440 is anticipated to resume at a later phase to 61 8 % projection of 0. 8440 to 0. 9041 from 0. 8902 at 0. 9273 Firm break there will pave the way to 0. 9375 vital framework resistance (2024 high) next.

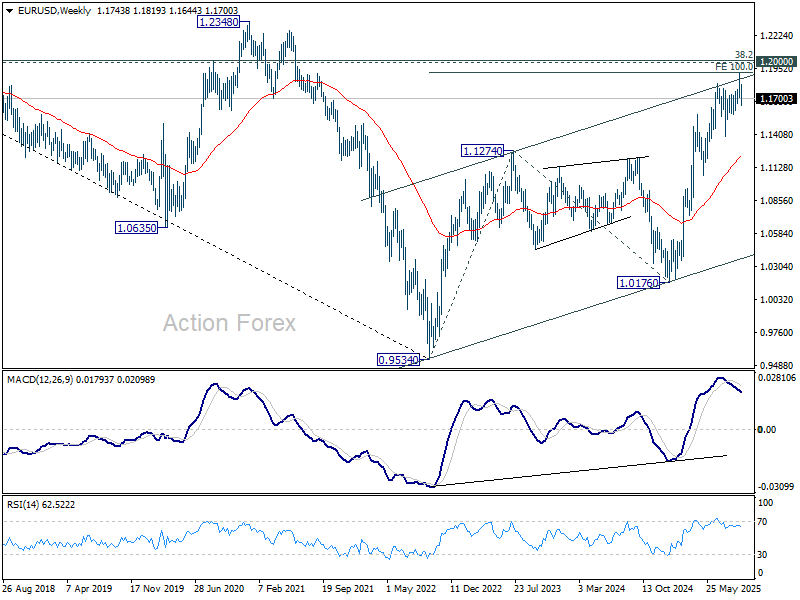

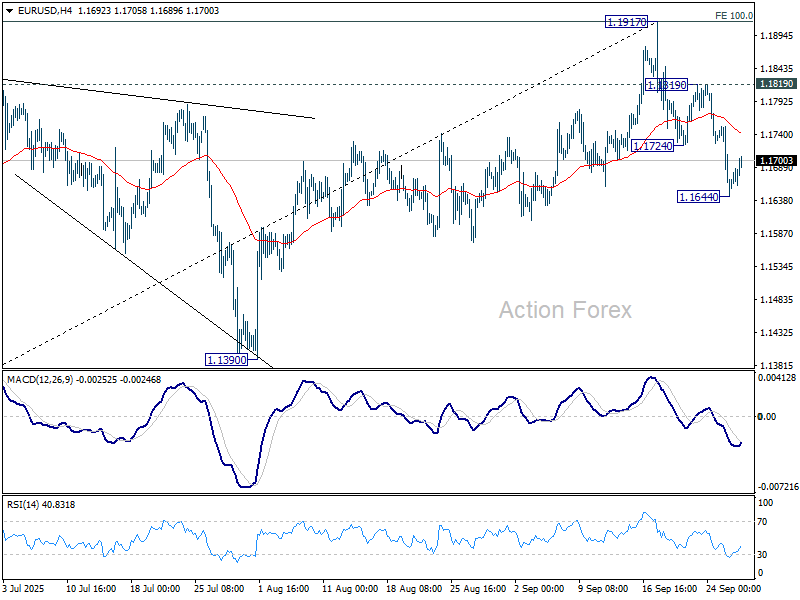

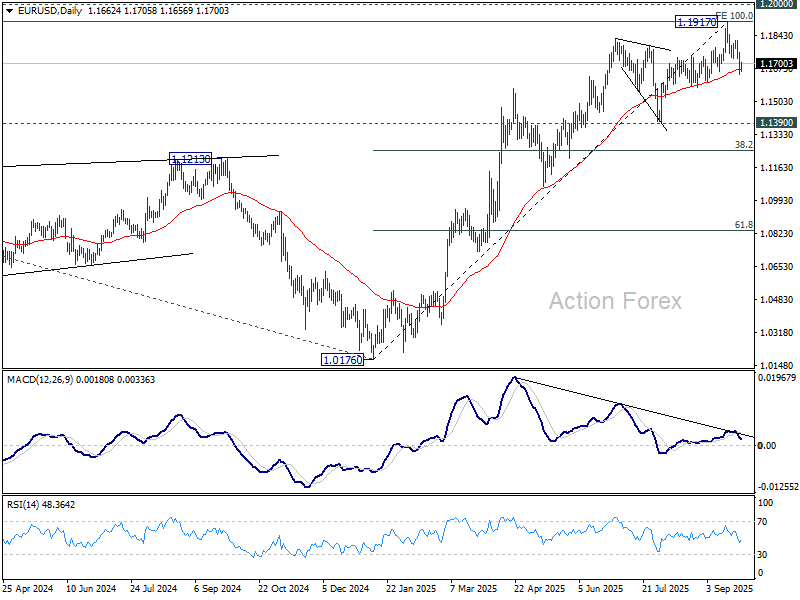

EUR/USD Weekly Outlook

EUR/USD’s loss from 1 1917 short term top extended to 1 1644 last week, however recuperated considering that once again. Initial predisposition is transformed neutral today first. Further fall is expected as long as 1 1819 resistance holds. Taking into consideration bearish aberration problem in D MACD, continual trading below 55 D EMA (currently at 1 1668 will say that 1 1917 was currently a medium term top. Much deeper loss must after that be seen to 1 1390 assistance following.

In the larger photo, surge from 1 0176 (2025 low) is viewed as the third leg of the pattern from 0. 9534 (2022 reduced). 100 % forecast of 0. 9534 to 1 1274 from 1 0176 at 1 1916 was already met. For now, further rally will stay in support as long as 1 1390 support holds, and firm break of 1 2000 mental degree will lug bigger favorable implications. However, company break of 1 1390 will recommend that surge from 1 0176 has already finished and bring deeper be up to 55 W EMA (now at 11231

In the long-term image, 38 2 % retracement of 1 6039 to 0. 9534 at 1 2019, which is close to 1 2000 emotional degree is the trick for the outlook. Rejection by this degree will certainly keep the multi years down fad from 1 6039 (2008 high) undamaged, and keep outlook neutral at ideal. Nevertheless, decisive break of 1 2000/ 19, will certainly suggest long term bullish fad turnaround, and target 61 8 % retracement at 1 3554