Markets went into recently with elevated anticipated and left with even sharper convictions. Weak united state labor data tilted sentiment emphatically toward faster Fed alleviating, while equity markets used that prospect as a springboard to yet an additional round of record highs.

Bond markets resembled that sight. US 10 -year yield broke quickly listed below 4 %, sending a signal that financiers prepare to front-load expectations for much deeper easing. In the currency markets, Dollar failed to recover ground, leaving the phase open for other majors to radiate.

At the front of the pack, Aussie rose in advance, powered in addition by strong local risk-on belief. Kiwi adhered to closely, while Sterling likewise took care of to climb, locating simply sufficient sustain to offset the weight of ongoing monetary concerns.

In raw comparison, Yen rotted as domestic threat hunger eclipsed the assistance from falling US returns. Loonie and Buck also slid to the bottom tier. In between, Euro and Swiss Franc gave a procedure of balance. Both profited modestly from Dollar weak point yet stopped short of major gains.

Wall Road Extends Document Run, 10 -Year Yield Presses 4 %

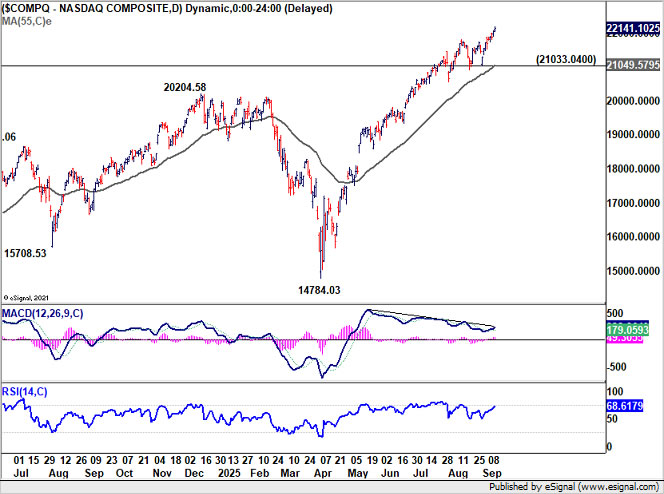

U.S. equities prolonged their uptrend last week, with all 3 significant indexes notching fresh document highs. NASDAQ led the cost, completing Friday at a new top, while S&P 500 tape-recorded its finest weekly performance considering that very early August and its 5th advance in six weeks. DOW slid somewhat on Friday however pleasantly held above the 46, 000 mark for the first time in history.

The rally was powered by strengthening conviction that the Fed will certainly increase its reducing cycle. Markets analyzed weak labor information– most notably the rise in first jobless claims to a four-year high– as verification that the economic climate requires added assistance. “Bad news was excellent news” for threat assets, with traders confident that the Fed will prioritize its employment required.

Inflation advancements included in the dovish mood. August’s CPI matched expectations and showed no fresh escalation in core pressures. PPI undershot forecasts, hinting that tariff-related boost may not be travelling through as boldy as feared. Integrated, the information enhanced the view that the Fed has space to cut without stiring inflationary dangers.

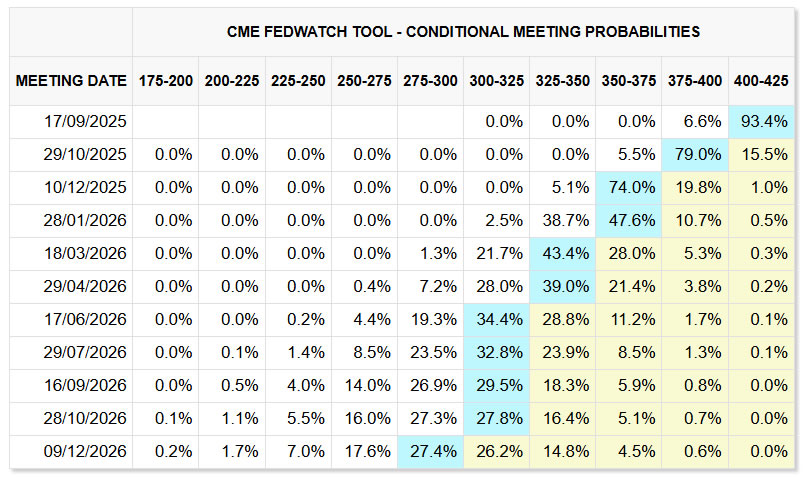

For the September 17 conference, a 25 bps price cut is totally priced in. Markets currently appoint roughly an 85 % likelihood to an additional relocate October and an 80 % chance of a December cut. If the Fed’s upgraded projections and Chair Jerome Powell’s remarks line up with this course, equities can find more gas for gains right into year-end.

Technically, NASDAQ is attempting to move far from its lasting ascending channel. Sustained trading above the resistance might set off a new age of acquiring, and press NASAQ to 100 % estimate of 10088 82 to 20204 58 from 14784 03 at 24899 78, which is close to 25 k emotional level.

On the various other hand, extended conditions are emerging in the stock exchange, as seen in overbought problem in W RSI, and bearish aberration condition in D MACD. Damage of 21033 04 support would certainly recommend the rally is tiring, opening the door for consolidation prior to any renewed press higher.

In set earnings, united state Treasuries additionally reflected the dovish tilt. 10 -year return dipped briefly to 3 996 before drawing support from close to term falling network, and recovered to near 4 061 %. While 10 -year yield might still attempt to protect the 4 % mental degree, any kind of recovery must be topped below 4 188 assistance transformed resistance.

The following directional relocation hinges on how the Fed structures its relieving cycle. A signal of faster cuts or a reduced incurable price would likely drive yields down additionally. Following target is 138 2 % forecast of 4 629 to 4 205 from 4 493 at 3 907, and even additionally at 161 8 % estimate at 3 807

Euro Slowness Limits Dollar Index Selloff

It was a classic bearish mixed drink for Buck last week– falling Treasury yields, strong threat hunger, and climbing assumptions for aggressive Fed easing. Yet Buck Index finished the week just marginally lower, indicating doubt amongst vendors in spite of the fundamental background. The biggest element avoiding a steeper Buck decline has actually been the slow-moving Euro. Normally Dollar’s most liquid equivalent, the solitary money has actually struggled to collect momentum.

Recently’s ECB conference gave no trigger, even though the Governing Council all maintained the down payment price unchanged at 2 00 % and President Christine Lagarde attempted to sound upbeat. Lagarde highlighted that threats to development had come to be “much more well balanced” complying with the U.S.– EU trade bargain that cut tariff unpredictability. She suggested that while higher tariffs, a more powerful Euro, and rising global competitors would evaluate on task this year, these headwinds need to discolor in 2026

Yet the narrative was drowned out by France’s getting worse political crisis. The ouster of Head of state François Bayrou highlighted the fragility of Head of state Emmanuel Macron’s federal government and revived fiscal sustainability concerns at once when long-term French returns are currently elevated. At the exact same time, Germany remains to deal with industrial despair.

Sentix capitalist confidence verified this fragile backdrop. The index dropped sharply in September to its weakest because April, with the survey blaming a harmful mix of French political instability, prolonged German weakness, an unfavorable tariff plan with the united state, and the war in Ukraine. It cautioned that the moderate summer season recovery in view had “disintegrated at a rapid pace” and saw long shot of an autumn rebound.

Versus this background, Euro’s inability to rally has actually blunted what could have been a more pronounced Buck selloff. Dollar Index remains to lean lower, however without Euro stamina, it lacks energy to break decisively through crucial support degrees.

Technically, as long as resistance at 98 63 caps rebounds, the close to term predisposition for Dollar Index is for an additional examination of 96 37 reduced. That level could hold on the initial attempt and activate a bounce.

Nonetheless, definitive break of 96 37 would to start with verify resumption of whole down pattern from 114 77 More notably, sustained trading below the multi-decade network floor at around 96 would certainly have major bearish ramifications. It would open deeper tool term down trend to 61 8 % retracement of 70 69 (2008 reduced) to 114 77 (2022 high) at 87 52

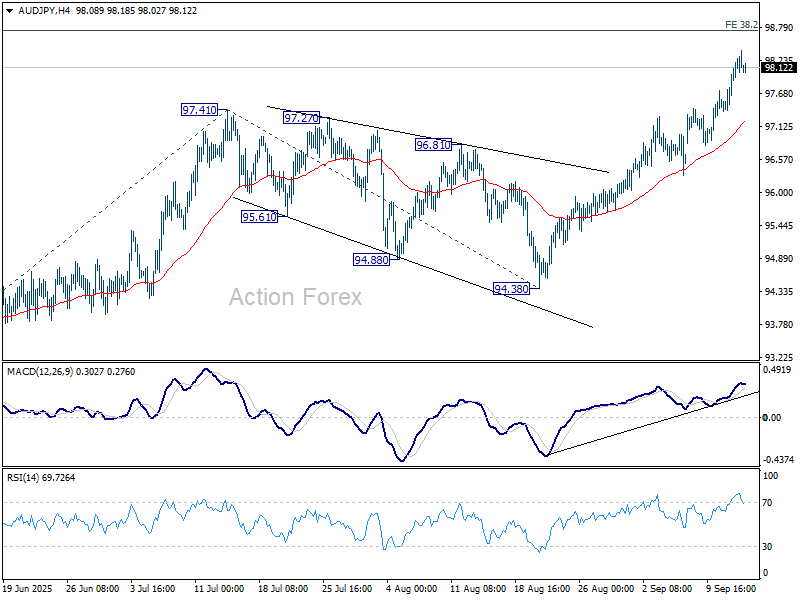

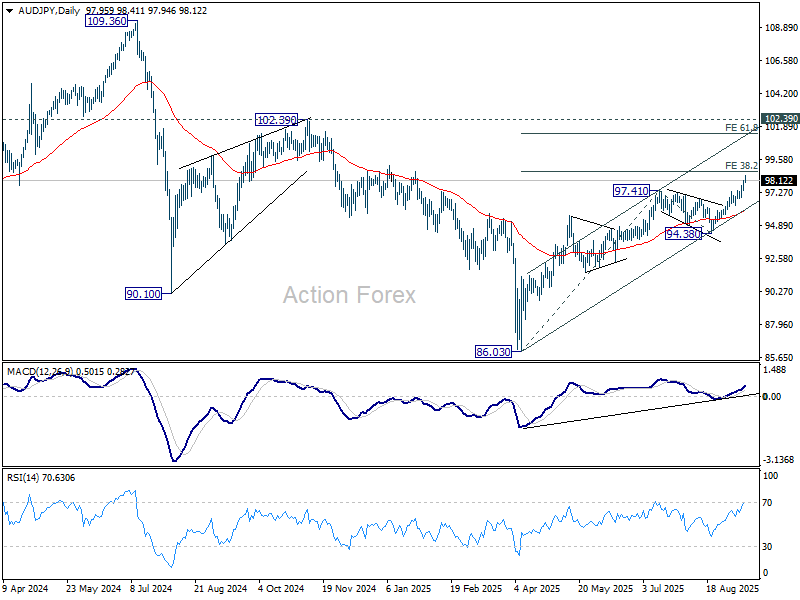

AUD/JPY Covers Weekly FX Performers Amidst Asia Equity Boom

Eastern stock markets likewise finished recently on a solid note, with favorable belief most obvious in Japan and Hong Kong. The mix of softer united state returns, installing Fed rate-cut expectations, and neighborhood stimulants produced powerful energy across the region, pushing indexes to multi-year and record highs.

In Tokyo, Nikkei rose greater than 4 % for the week, marking yet an additional record. The rally was fueled by multiple variables: Technology and AI-linked shares tracking NASDAQ’s toughness, optimism over Fed easing, and restored political hopes at home. The development of previous financial safety and security minister Sanae Takaichi as a frontrunner for the LDP presidency infused a distinctively residential bullish element, as capitalists searched for a potential return to Abenomics-style policies favoring financial assistance and financial holiday accommodation.

Trade advancements included an additional tailwind. Japan lately safeguarded a reduction in U.S. car tolls, easing a critical stress point for the nation’s vital export field. Together, these drivers made for an uncommon alignment of worldwide and neighborhood positives, giving the Nikkei its greatest weekly performance in months.

Technically, Nikkei stays on course to 100 % estimate of 25661 89 to 42426 77 from 30792 74 at 47557 62 Expectation will remain bullish as long as 41863 20 support holds, in instance of resort.

Hong Kong’s Hang Seng Index additionally excited, uploading its largest weekly gain in 6 months and closing at the highest level because August 2021 The rally was supported by boosting liquidity conditions, along with the prospect that an U.S. price cut could motivate individuals’s Bank of China to alleviate policy additionally. Such an action might motivate mainland savers to revolve deposits into equities, boosting evaluations.

Furthermore Hong Kong stocks continue to be underestimated relative to mainland peers, which recently rallied to years highs. With added “southbound inflows” from mainland capitalists utilizing the stock attach program, liquidity conditions are likely to stay encouraging, feeding positive outlook that the HSI still has room to catch up.

Technically, HSI gets on track in the direction of 161 8 % projection of 14597 31 to 22700 85 from 14794 16 at 27905 69 For the close to term, outlook will certainly stay bullish as long as 25013 26 support holds, in instance of hideaway.

In currency markets, the risk-on tone spilled over in the region. AUD/JPY emerged as the week’s best-performer, closing 1 59 % greater. Immediate focus is now on 38 2 % estimate of 86 03 to 97 41 from 94 38 at 98 72 Firm break there will certainly lead the way to 61 8 % forecast at 101 41 next. Nonetheless, break of 97 38 support will certainly bring debt consolidations initially, before presenting an additional surge.

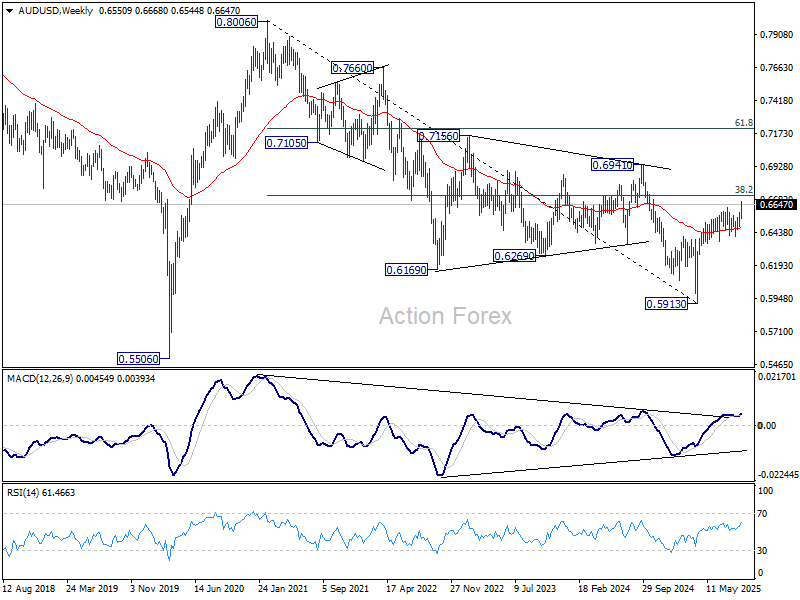

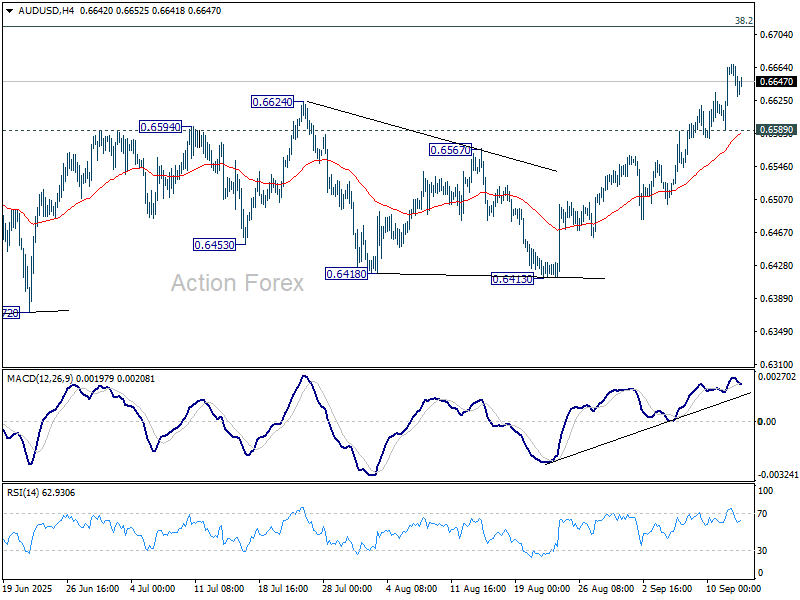

AUD/USD Weekly Report

AUD/USD’s rise from 0. 5913 resumed with 0. 6624 resistance recently. There is no sign of topping yet, and first prejudice remains on the benefit. Next target is 0. 6713 fibonacci level. Company break there will certainly lug bigger bullish implications. On the drawback, listed below 0. 6589 small assistance will certainly turn prejudice neutral and bring consolidations first, before presenting another rally.

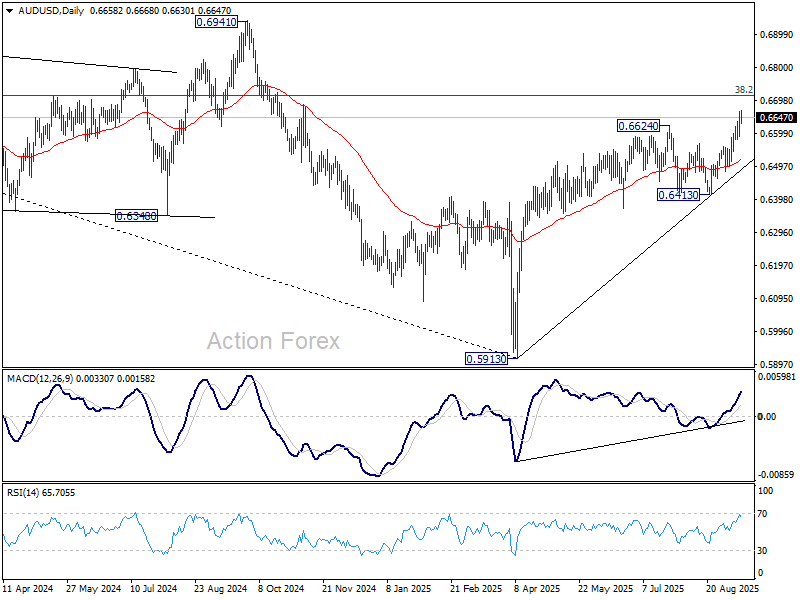

In the larger picture, there is no clear indication that down fad from 0. 8006 (2021 high) has actually finished. Rebound from 0. 5913 is viewed as a corrective move. While more powerful rally can not be dismissed, expectation will certainly stay bearish as long as 38 2 % retracement of 0. 8006 to 0. 5913 at 0. 6713 holds. Nevertheless, taking into consideration favorable merging problem in W MACD, sustained break of 0. 6713 will certainly be a strong indication of bullish trend turnaround, and path the means to 0. 6941 architectural resistance for verification.

In the long term picture, loss from 0. 8006 is seen as the 2nd leg of the corrective pattern from 0. 5506 long-term base (2020 reduced). Thus, in case of deeper decline, strong support ought to emerge over 0. 5506 to include downside to bring reversal. On the advantage, firm break of 0. 6941 will certainly argue that the 3rd leg has actually already drawn back to 0. 8006